Documents Required for ITR Filing: A Complete FY 2025-26 Checklist

Introduction

Filing an Income Tax Return becomes much easier when all relevant documents are organised before you begin. Many taxpayers start filing with only Form 16 and later realise that bank interest certificates, AIS entries, investment proofs, rent documents, tax challans or capital gains statements are missing.

A well-prepared ITR filing checklist helps you report income correctly, reconcile TDS and TCS, avoid missing deductions, and reduce the chances of refund delays or follow-up notices. Whether you are a salaried employee, freelancer, investor, landlord or taxpayer with foreign income, knowing what to keep ready makes the filing process more systematic. Since the due date for filing your ITR for AY 2026-27 (income of FY 2025-26) is July 31, 2026, get started now.

Essential Documents Required for ITR Filing

Every taxpayer may not need the same records. However, certain documents required for ITR filing are relevant across most categories of taxpayers.

- PAN, Aadhaar and e-filing Portal Details

Your PAN is the primary identifier for income tax filing. Aadhaar is also important for authentication, e-verification and profile matching. Before filing, check whether your name, date of birth, PAN, Aadhaar, mobile number and email ID are correctly updated on the income tax portal.

You should also keep your e-filing portal credentials ready. If you plan to verify your return through Aadhaar OTP, make sure your mobile number is linked with Aadhaar.

2. Bank Account Details

Keep details of all active bank accounts ready, including account number, IFSC, bank name and account type. For refunds, at least one bank account should be pre-validated and nominated on the e-filing portal. The Income Tax Department’s ITR-2 manual also recommends pre-validating at least one bank account and nominating it for refund. (Income Tax India)

Bank statements are also useful for checking salary credits, professional receipts, rent received, interest income, dividend credits, tax payments and other transactions.

3. Form 16 From Employer

Form 16 is one of the key documents required for salaried employees to file ITR. It shows salary income, exemptions, deductions and tax deducted by the employer during the financial year.

If you changed jobs during the year, collect Form 16 from each employer. Also keep salary slips, full-and-final settlement details, bonus details, leave encashment details, gratuity details and arrear salary information, if applicable.

4. Form 26AS, AIS, and TIS

Form 26AS, AIS and TIS should be reviewed together before filing. Form 26AS is mainly used to verify TDS and TCS details. The Income Tax Department states that from AY 2023-24 onward, Form 26AS available on TRACES displays only TDS/TCS-related data, while other taxpayer information is available in AIS. AIS also allows taxpayers to provide feedback on reported transactions. (Income Tax India)

AIS gives a broader view of reported financial information, such as interest, dividends, securities transactions and other reported activities. TIS gives a category-wise summary of this information.

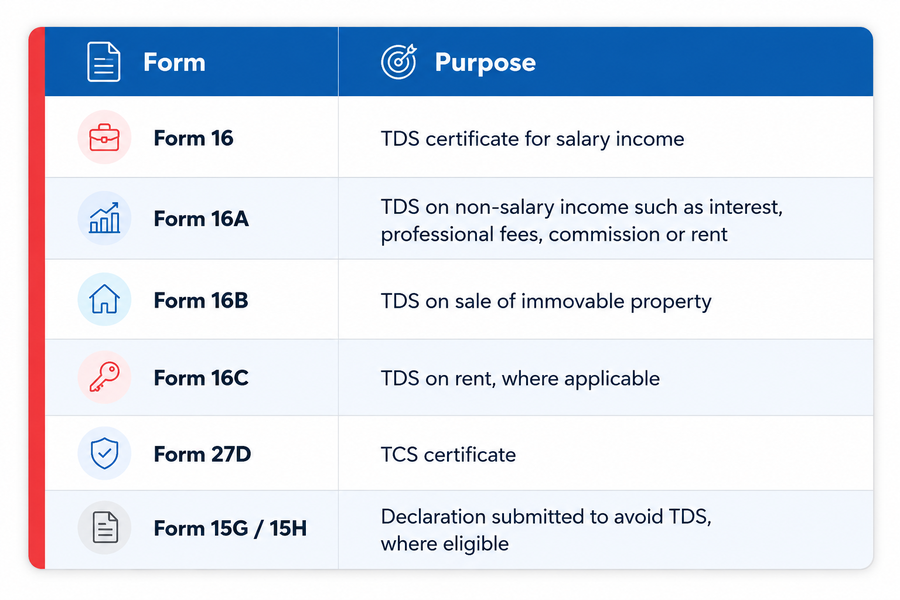

5. TDS and TCS Certificates

Depending on your income type, you may need more than Form 16. Keep these ready where applicable:

The Income Tax Department’s ITR-2 FAQ mentions Form 16, Form 16A, Form 26AS, rent receipts, capital gains statements and other records that taxpayers may need while filing. (Income Tax India)

- Tax Payment Challans

If you paid advance tax or self-assessment tax, keep the challan details ready. Check the assessment year, challan amount, BSR code, challan number and payment date.

The ITR-2 user manual states that the “Tax Paid” section requires taxpayers to verify TDS from salary, TDS from income other than salary, TCS, advance tax and self-assessment tax. (Income Tax India)

2. Bank Interest and Investment Income Records

Savings account interest, fixed deposit interest, recurring deposit interest, dividend income and other investment income should be reported even where TDS has not been deducted. Keep these documents ready:

- Bank interest certificates

- Fixed deposit receipts

- Bank statements

- Dividend statements

- Mutual fund statements

- Broker reports

- Post office interest certificates

- Bond or debenture interest statements

Although income is reported on the AIS, bank records should still be reviewed for reconciliation and completeness. In fact, taxpayers should reconcile all documents, including Form 16 and Form 26AS before filing to reduce chances of receiving a notice from the IT Department and avoid penalties.

ITR Filing Checklist Based on Income Source

Beyond the common documents required for ITR filing, additional records may be necessary depending on whether you are salaried, a professional or freelancer, or have income as a result of investments or giving a house on rent. Take a look below:

A. Salaried Individuals

Salaried taxpayers should keep these documents ready:

- Form 16 from all employers

- Salary slips

- Form 12BB submitted to employer

- Form 16A, where applicable

- Form 26AS, AIS and TIS

- Bank statements showing salary credits

- Bonus, incentive, gratuity, leave encashment or severance details

- Form 10E acknowledgement, if claiming relief for salary arrears

- Rent receipts and rent agreement for HRA

- Home loan certificate, if claiming home loan benefits

- Investment and insurance proofs, if using the old tax regime

A common mistake is missing salary from a previous employer. Always compare Form 16, AIS and bank statements before finalising the return.

B. Freelancers and Professionals

Freelancers, consultants, and professionals should prepare income and expense records before filing. Here are the documents required for freelancer ITR filing and other similar professions:

- Invoices raised during the year

- Client-wise income summary

- Bank statements for professional receipts

- Form 16A for TDS deducted by clients

- AIS and Form 26AS for TDS reconciliation

- Expense bills for internet, software, subscriptions, rent, utilities, travel and equipment

- GST returns, if registered

- Books of accounts or income-expense statement

- Presumptive taxation working, if applicable

- Advance tax and self-assessment tax challans

- Tax audit report, if applicable

Taxpayers with business or professional income may need ITR-3 or ITR-4, depending on their income profile and eligibility.

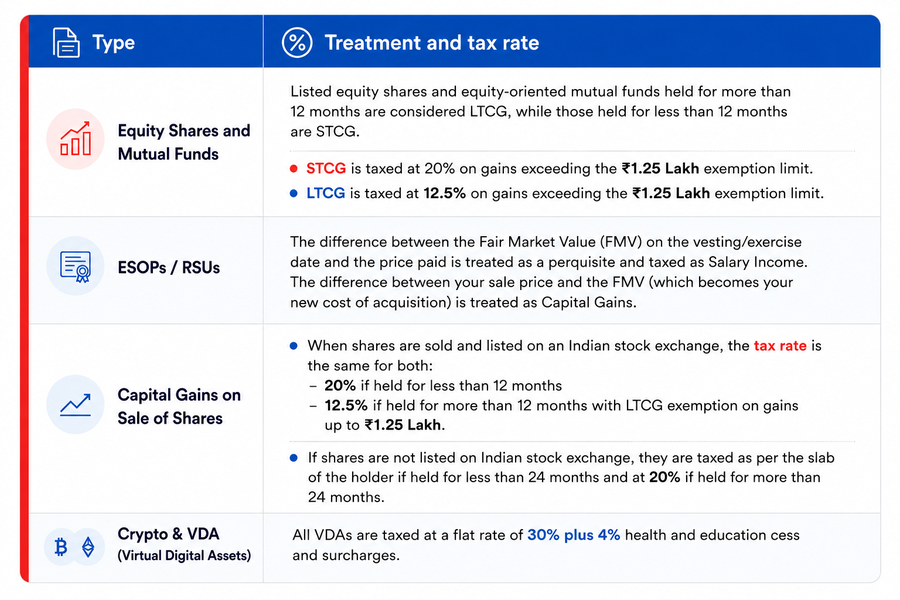

C. Investors and Capital Gains Taxpayers

If you sold shares, mutual funds, property, bonds, debentures or virtual digital assets, you need capital gains documents for ITR filing. Keep these documents ready:

- Broker profit and loss statement

- Contract notes

- Demat account statement

- Mutual fund capital gains statement

- Consolidated Account Statement, where available

- Purchase and sale dates

- Cost of acquisition and sale consideration

- STT details, where applicable

- Property purchase deed and sale deed

- Stamp duty value, brokerage details and improvement cost proofs

- Form 16B, if TDS was deducted on property sale

- Crypto or VDA exchange statements and transaction-wise purchase/sale details

The ITR-2 manual notes that Schedule Capital Gains captures short-term and long-term capital gains or losses. It also states that scrip-wise details are mandatory in specified cases under Schedule 112A where shares were bought on or before January 31, 2018.

Here’s a quick look at how popular investments are taxed:

D. House Property Income

Taxpayers with self-occupied, let-out or deemed let-out property should keep property-related records ready.

Documents include:

- Rent agreement

- Rent receipts

- Tenant details

- Municipal tax receipts

- Home loan interest certificate

- Principal repayment certificate

- Co-owner details and ownership share

- Property purchase documents

- Rent received details

- Vacancy period details, if applicable

The ITR-2 manual states that Schedule House Property includes details for self-occupied, let-out and deemed let-out property, including co-owner details, tenant details, rent and interest.

E. Foreign Income, Foreign Assets, and NRI-related Income

Taxpayers with foreign income or assets should be careful about selecting the right ITR form and reporting the right schedules. Keep these documents ready:

- Foreign bank statements

- Foreign brokerage statements

- Foreign salary slips or tax statements

- RSU or ESOP vesting and sale statements

- Foreign tax paid certificates

- Foreign dividend, interest or capital gains records

- Form 67 details, if claiming foreign tax credit

- Schedule FA, Schedule FSI and Schedule TR details

- NRE and NRO bank interest certificates for NRIs

- DTAA-related supporting documents, where applicable

The ITR-2 user manual states that Schedule FA is used to provide details of foreign assets or income from any source outside India.

F. Taxpayers Who May Need Schedule AL

Schedule AL is generally applicable where total income exceeds ₹1 crore and the taxpayer is filing a return requiring Schedule AL disclosure. In the notified ITR-2 form, Schedule AL applies where total income exceeds ₹1 crore; in ITR-3, Schedule AL applies where total income exceeds ₹1 crore and covers assets other than those included in Part A-BS.

Keep these details ready where applicable:

- Immovable property details

- Bank balances

- Shares and securities

- Insurance policies

- Loans and advances given

- Cash in hand

- Jewellery, bullion, vehicles and other reportable movable assets

- Liabilities linked to reported assets

Documents Needed for Deductions and Tax Regime Selection

Before claiming deductions, compare the old and new tax regimes. The Income Tax Department explains that the old regime allows various deductions and exemptions, while the new regime offers lower rates with limited deductions and exemptions.

Under the new tax regime, resident individuals may effectively have no tax liability up to taxable income of ₹12 lakh due to the enhanced rebate under Section 87A, subject to conditions and excluding income taxable at special rates such as certain capital gains.

The Income Tax Department’s Finance Act 2025 highlights state that the Section 87A rebate threshold for resident individuals under the new regime was increased from ₹7 lakh to ₹12 lakh, with the maximum rebate increased from ₹25,000 to ₹60,000. The PIB also notes that the “no tax” benefit excludes special-rate income such as capital gains.

If the old regime is beneficial, keep these deduction and exemption proofs ready.

80C Deduction Proofs

- EPF contribution details

- PPF passbook

- ELSS investment statement

- Life insurance premium receipts

- Tuition fee receipts

- NSC investment proof

- Home loan principal repayment certificate

80D Deduction Proofs

- Health insurance premium receipts

- Preventive health check-up bills

- Senior citizen medical expense records, where applicable

- Policy number and insurer details

NPS Documents

- NPS contribution receipt

- PRAN

- Employer NPS contribution details, where applicable

Donation Documents

- Donation receipt

- Donee name, PAN and registration details

- Mode of payment

- Form 10BE, where applicable

Rent and Home Loan Documents

- Rent receipts

- Rent agreement

- Landlord details

- Home loan interest certificate

- Loan account statement

- Possession or completion certificate, where applicable

- Co-owner details, if applicable

Common Documentation Gaps That Can Affect ITR Filing

Many filing issues arise not because documents are unavailable, but because taxpayers do not compare or check them before filing. Here are a few common gaps that you must review before filing your ITR:

- Missing Form 16 from a previous employer

- Reporting only Form 16 income and ignoring AIS/TIS

- Not reporting savings account interest or FD interest

- Missing dividend income

- Missing Form 16A for non-salary TDS

- Not reconciling Form 26AS with claimed TDS

- Selecting the wrong ITR form

- Missing rent receipts or landlord details for HRA

- Claiming deductions under the wrong tax regime

- Not keeping home loan interest certificates

- Missing Form 10E for salary arrears

- Not reporting capital gains correctly

- Not reporting foreign assets or income

- Missing Form 67 while claiming foreign tax credit

- Not checking Schedule AL applicability

- Filing but not e-verifying the return

How to Prepare Before Filing Your ITR

When taxpayers ask what to keep ready before filing ITR, the answer is not a single document. It is a combination of income records, tax statements, deduction proofs, and verification documents that together provide a complete picture of the financial year. Once you have them handy, follow these steps:

Step 1: Confirm the Filing Year and ITR Form

Confirm the correct assessment year once, then choose the applicable ITR form based on your income type, residential status and reporting requirements.

Step 2: Download Form 26AS, AIS, and TIS

Compare these statements with your salary records, bank statements, investment records and TDS certificates. AIS may contain broader financial transaction data, while Form 26AS primarily helps verify TDS/TCS-related information.

Step 3: Reconcile Income from All Sources

Add salary, freelance income, business income, rent, interest, dividend, capital gains, foreign income and exempt income. Do not rely only on Form 16.

Step 4: Compare Old and New Tax Regimes

Check tax liability under both regimes before filing. Some deductions and exemptions are available only under the old regime, while the new regime has limited deductions and exemptions.

Step 5: Verify Tax Credits

Check whether all TDS, TCS, advance tax and self-assessment tax payments are correctly reflected. If TDS is missing, contact the employer, bank, client or deductor before filing.

Step 6: Validate Bank Account Details

Make sure the refund bank account is active, correctly entered and pre-validated on the e-filing portal.

Step 7: Review the Return Before Submission

Check the following to avoid delays or issues:

- Gross total income

- Deductions

- Taxable income

- Special-rate income

- TDS/TCS credits

- Advance tax

- Self-assessment tax

- Refund or tax payable

- Bank account nominated for refund

Step 8: E-verify After Filing

Return filing is not complete until the ITR is verified. The Income Tax Department states that without verification within the stipulated time, an ITR is treated as invalid. The 30-day ITR-V guidance also explains the consequences where e-verification or ITR-V submission is completed after the timeline.

How Zaggle’s Tax Solution Helps

For employees and organisations, ITR-related documentation often involves multiple moving parts: salary records, investment proofs, declarations, TDS details, Form 16, AIS/TIS review, deduction planning and filing support.

Zaggle’s Tax Solution delivers a combined view of AIS, TIS, and Form 26AS information, helping users detect discrepancies between reported income and tax credits before filing. It also simplifies reconciliation by tracking income across multiple sources, making it easier to review records before preparing returns.

In addition, it supports tax and compliance workflows such as bulk proof verification, salary restructuring, income tax return filing and review, GST return filing, TDS computation and reconciliation, and compliance-ready reporting.

A structured tax workflow can help organisations:

- Collect and organise employee tax documents

- Reduce manual follow-ups during proof submission

- Review TDS and deduction-related records more systematically

- Maintain compliance-ready documentation

- Support employees through guided filing and review processes

- Handle notices, assessments and follow-ups with better record availability

Zaggle also connects users with CAs and tax experts to help reduce filing errors and simplify return preparation. For taxpayers, this can make the filing process easier by keeping records, declarations and filing support in a more organised flow. For payroll and finance teams, it can reduce repetitive manual work and improve visibility across tax-related processes.

Conclusion

A complete ITR filing checklist is not only about collecting documents. It helps you report income correctly, reconcile tax credits, compare tax regimes, claim eligible deductions and reduce filing errors.

Before filing, keep your identity details, salary records, Form 26AS, AIS, TIS, bank statements, investment proofs, tax challans, capital gains records and deduction documents ready. Since ITRs are generally annexure-less, you may not upload these documents with the return, but you should retain them safely for future reference.

Frequently Asked Questions

- What are the most important documents required for ITR filing?

The most important documents include PAN, Aadhaar, Form 16, Form 26AS, AIS, TIS, bank statements, Form 16A where applicable, tax payment challans, investment proofs, capital gains statements and deduction-related documents.

2. Do I need to upload documents while filing ITR?

Usually, no. ITR forms are annexure-less, so documents such as proof of investment and TDS certificates are not attached with the return. However, taxpayers should keep them for assessment, inquiry or verification.

3. Is Form 16 mandatory for filing ITR?

Form 16 is very useful for salaried taxpayers, but if it is not available, you may still be able to file using salary slips, bank statements, AIS, Form 26AS and other salary records. However, salary and TDS details should be reconciled carefully.

4. What should I do if AIS and Form 26AS do not match?

Check the difference line by line. AIS may show wider financial information, while Form 26AS mainly reflects TDS/TCS-related data. If AIS shows incorrect information, use the AIS feedback option. If TDS is missing in Form 26AS, contact the deductor.

5. Which documents are needed for HRA?

Keep rent receipts, rent agreement, landlord details and rent payment proofs ready. HRA exemption is generally relevant when filing under the old tax regime.

6. Which documents are required for capital gains?

You may need broker statements, contract notes, demat statements, mutual fund capital gains reports, property purchase and sale deeds, improvement cost proofs, stamp duty value and Form 16B, where applicable.

7. What documents are needed for freelancers?

Freelancers should keep invoices, client-wise receipts, bank statements, Form 16A, AIS, Form 26AS, expense bills, GST returns where applicable, books of accounts and advance tax challans.

8. When does Schedule AL apply?

Schedule AL is generally applicable where total income exceeds ₹1 crore and the taxpayer is filing a return that requires Schedule AL disclosure. The notified ITR-2 and ITR-3 forms for the relevant year include Schedule AL with the ₹1 crore threshold.

9. How soon should I e-verify my ITR?

You should e-verify your ITR within the stipulated timeline after filing. If the return is not verified within the required time, it may be treated as invalid. Organising your records before filing can make the process faster, cleaner and more accurate.

Explore TaxSpanner's wide range of calculators for your tax planning and calculations!

View Tools & Calculators