Tax Deductions Breakdown: 80C, 80D, HRA, EV, Home Loan & More

It’s the end of August 2025, and the ITR deadline is approaching. Like every year, you’re reminded of how much tax is deducted from your salary. It often feels like your money just comes and disappears. You may have heard friends or colleagues discussing tax-saving tips, deductions, or exemptions, but it can seem quite confusing.

But the truth is, saving on taxes doesn’t have to be hard. There are simple, legal ways to lower your tax liability. Once you understand the basics, it actually becomes easier with each passing year. It’s about knowing where you can save and making small, smart choices that keep more money in your pocket.

This article will guide you through some deduction options that can help you save on taxes.

Income Tax Deductions Under Section 80C

- Section 80C is a popular section for tax savings, allowing a maximum deduction of Rs.1,50,000. This section covers various investments and expenses, including:

- Principal Repayment of Home Loan: You can claim a deduction of up to Rs.1,50,000 for the principal repaid on a home loan. To qualify, the loan must be for buying or building a new house, and you can’t sell the property within 5 years of ownership. If you sell before 5 years, the previously claimed deductions will be added back to your income. This limit also includes costs for stamp duty, registration, and transfer expenses related to the property.

- Other common investments under 80C include contributions to EPF, PPF, ELSS, life insurance premiums, children's tuition fees, NPS (employee contribution), Sukanya Samriddhi Yojana, and senior citizen deposits.

FILE NOW

Tax Deductions Under Section 80D: Health Insurance Premiums

- Section 80D provides deductions for health insurance premiums that are paid to insurance companies to promote health and financial security. This deduction is mostly available to those under the old tax regime. Most taxpayers choosing the new tax regime are not eligible to claim 80D deductions.

Deduction Limits:

- You can claim up to Rs.25,000 for premiums paid for yourself, your spouse, and dependent children.

- For premiums paid for parents, you can claim an additional Rs.25,000. If your parents are senior citizens (over 60 years old), this amount can increase up to Rs.50,000.

- You can also include preventive health check-ups up to Rs.5,000 in this overall limit.

To optimize 80D Deductions, consider following these steps:

- Consider taking family floater plans to cover several family members within the Rs.25,000 limit.

- For senior citizen parents, consider separate policies to take advantage of their higher deduction limit of Rs.50,000.

Don’t forget to include preventive health check-up costs to increase your claim. - Always pay premiums on time and keep payment proofs and receipts easily accessible.

FILE NOW

Section 24 - Tax Deductions on Home Loan Interest

- This section provides a deduction on the interest portion of your home loan. You can claim up to Rs.2,00,000 on home loan interest if the house is self-occupied or vacant.

Eligibility Criteria for Rs.2,00,000 Deduction:

- The loan must have been taken on or after April 1, 1999.

- The purchase or construction must be completed within 3 years from the end of the financial year in which the loan was taken.

- The loan's purpose must be buying or constructing a new house.

- Reduced Deduction: If you don't meet the above criteria or if the loan is for reconstruction, renewal, or repair, the maximum deduction is capped at Rs.30,000.

- Rented Property: If the house is rented out, you can claim the entire home loan interest as a deduction, subject to specific income tax rules on house property income.

- Pre-construction Interest: Interest paid during pre-construction (before the property is finished) can be claimed in five equal installments starting from the financial year when construction is completed. No deductions can be claimed while the house is still under construction.

FILE NOW

Home Loan Tax Benefits for Women Homebuyers

Under the old tax regime, women co-owners of a joint home loan can each claim benefits of up to Rs.1.5 lakh per year on the principal (under Section 80C) and up to Rs.2 lakh each on the interest paid (under Section 24).

Home Loan Tax Benefits for Senior Citizens

Senior citizens (60-80 years) and super senior citizens (above 80 years) can also enjoy home loan tax benefits, provided they meet the age criteria during the financial year.

House Rent Allowance (HRA) Exemption

- HRA is a part of your salary that helps cover your rent and also provides a tax exemption under Section 10(13A).

- Eligibility: You must be a salaried employee living in a rented home, and HRA must be part of your salary (CTC). You also need to submit valid rent receipts.

- Exemption Calculation: The HRA exemption depends on factors like your salary, actual rent paid, HRA received, and your city of residence.

- Important Note: If you live in your own property, the HRA you receive is fully taxable.

Other Important Deductions Available in FY 2025

Unlike older deductions such as Section 80EE (first-time homeowners) or 80EEB (electric vehicle loans), which are no longer relevant for most taxpayers today, the following remain key under the old tax regime:

- Section 80G: Deduction for donations made to eligible charitable institutions and funds.

- Section 80E: Deduction on interest paid for education loans (available for higher education in India or abroad).

- Section 80CCD(1B): Additional deduction of Rs.50,000 for contributions made to the National Pension System (NPS).

- Leave Travel Allowance (LTA): Tax exemption for travel expenses within India, subject to conditions.

FILE NOW

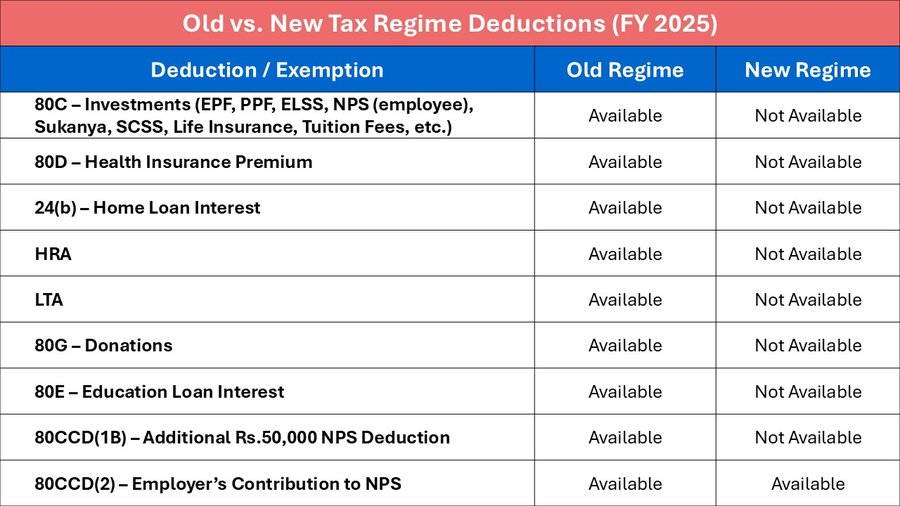

Important Note on Regimes: All deductions like 80C, 80D, 80G, 80E, 80CCD(1B), HRA, LTA are available only under the old tax regime.

The only deduction available under both old and new regimes is 80CCD(2) – the employer’s contribution to NPS.

Conclusion

Understanding these income tax deductions is key for effective tax planning in 2025. Whether it’s maximizing benefits under Section 80C for investments and home loan principal payments, using Section 80D for health insurance, or taking advantage of exemptions under HRA, LTA, and donations under Section 80G, strategic planning can lead to significant tax savings. Keep in mind whether you fall under the old or new tax regime, as eligibility for certain deductions can vary. You can also use a tax calculator or consult an expert at Taxspanner for assistance.

Explore TaxSpanner's wide range of calculators for your tax planning and calculations!

View Tools & Calculators